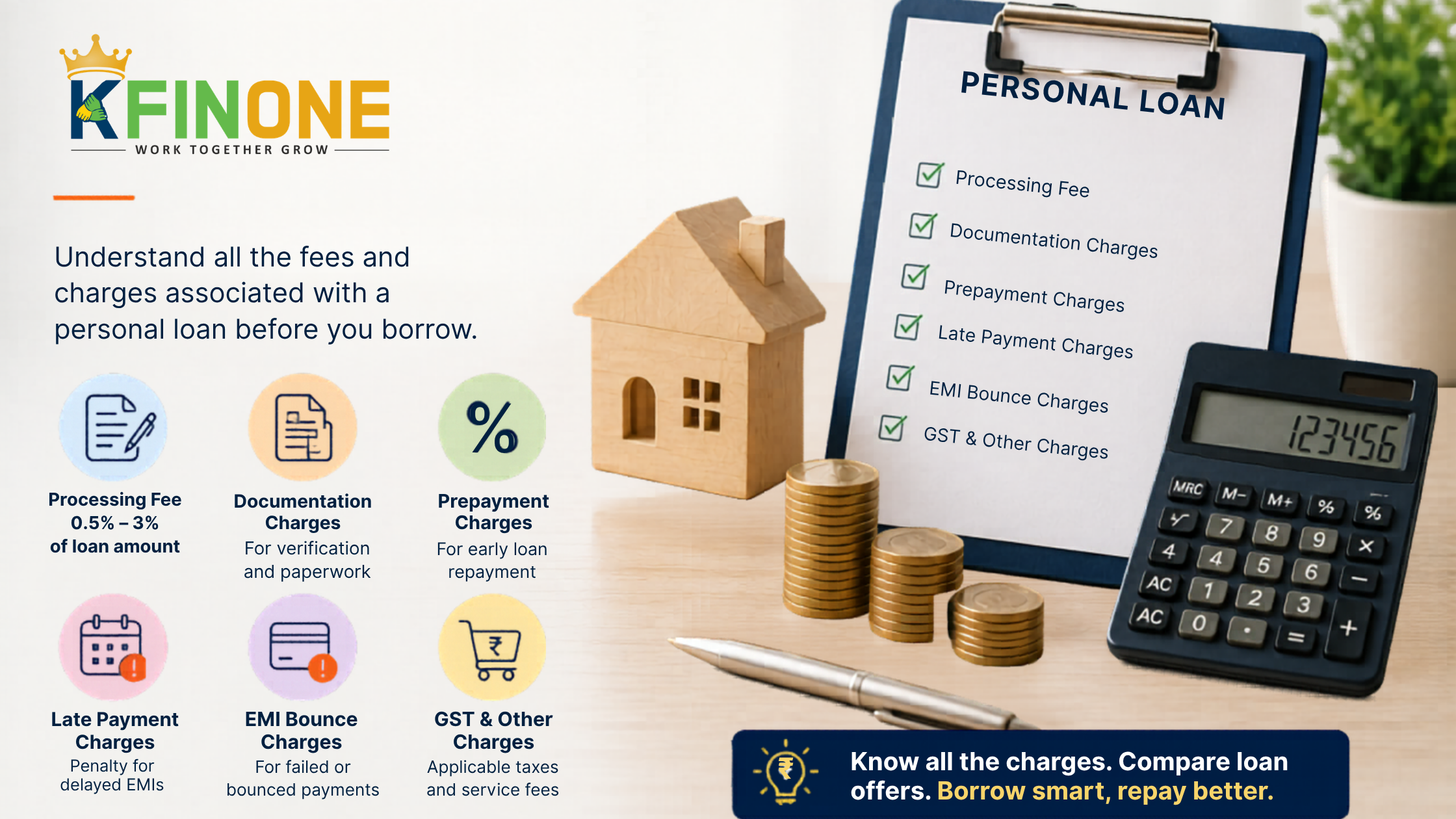

What is the Processing Fee & Charges for a Personal Loan?

Personal loans are one of the most convenient financial solutions for managing unexpected expenses, medical emergencies, education costs, home renovations, travel plans, or debt consolidation. While borrowers often focus on interest rates and loan amounts, it is equally important to understand the processing fees and other charges associated with a personal loan. These costs can impact the overall borrowing expense and should be considered before applying.

Understanding Personal Loan Processing Fees

A processing fee is a one-time charge collected by the lender for evaluating, verifying, and processing a loan application. This fee covers administrative expenses such as document verification, credit assessment, eligibility checks, and loan approval procedures.

Most lenders charge a processing fee as a percentage of the sanctioned loan amount. Depending on the lender, this fee may range from 0.5% to 3% of the loan value, along with applicable taxes.

For example, if you apply for a personal loan of ₹5,00,000 and the lender charges a 2% processing fee, the fee would be ₹10,000 plus applicable taxes.

Why Do Lenders Charge a Processing Fee?

Processing fees help lenders cover the costs involved in:

- Verifying applicant details

- Reviewing credit history

- Assessing repayment capacity

- Conducting risk analysis

- Managing documentation

- Disbursing the loan amount

These procedures ensure that the lender can evaluate the borrower's eligibility and repayment ability before approving the loan.

Common Charges Associated with Personal Loans

Apart from the processing fee, borrowers may encounter several other charges during the loan tenure.

1. Documentation Charges

Some lenders may charge fees for document verification and legal formalities. These charges are generally included in the processing fee but may occasionally be charged separately.

2. Prepayment or Foreclosure Charges

Borrowers who wish to repay the loan before the tenure ends may be subject to prepayment or foreclosure fees. These charges compensate lenders for the loss of future interest income.

The fee is usually calculated as a percentage of the outstanding loan balance.

3. Late Payment Charges

If an EMI payment is delayed or missed, lenders may impose a penalty. Late payment charges can increase the overall cost of borrowing and may negatively affect the borrower's credit score.

4. EMI Bounce Charges

When an EMI payment fails due to insufficient bank balance or transaction failure, lenders often levy bounce charges for each unsuccessful transaction.

5. Loan Cancellation Charges

If a borrower decides to cancel the loan after approval or disbursement, certain cancellation fees may apply depending on the lender's policy.

6. Statement or Account Maintenance Charges

Some lenders charge fees for issuing duplicate loan statements, repayment schedules, or account-related services.

7. GST and Applicable Taxes

Processing fees and various service charges are usually subject to Goods and Services Tax (GST), which further increases the overall cost.

How is the Processing Fee Deducted?

In most cases, the processing fee is deducted from the sanctioned loan amount before disbursement.

For example:

- Approved Loan Amount: ₹3,00,000

- Processing Fee: ₹6,000

- GST on Fee: Applicable

- Amount Received by Borrower: Loan Amount minus charges

Therefore, borrowers may receive slightly less than the approved loan amount.

Factors That Influence Processing Fees

Several factors determine the processing fee charged by lenders:

Loan Amount

Higher loan amounts may attract higher processing fees.

Applicant Profile

Credit score, income level, employment stability, and repayment history may influence lender charges.

Lender Policies

Different financial institutions follow different fee structures and promotional offers.

Special Offers

During festive seasons or promotional campaigns, some lenders may offer reduced or zero processing fees.

Tips to Reduce Personal Loan Charges

Compare Multiple Lenders

Review processing fees, interest rates, and additional charges before selecting a lender.

Maintain a Good Credit Score

A strong credit profile may help secure better loan terms and lower fees.

Read the Loan Agreement Carefully

Always review the fee structure, penalty clauses, and repayment conditions before signing.

Ask About Hidden Charges

Clarify all applicable costs including foreclosure fees, EMI bounce charges, and service fees.

Look for Promotional Offers

Many lenders provide discounts on processing fees during special campaigns.

Importance of Understanding Loan Charges

A lower interest rate does not always mean a cheaper loan. Processing fees and additional charges can significantly affect the total borrowing cost. Understanding every fee associated with a personal loan helps borrowers make informed decisions and avoid unexpected expenses.

Carefully comparing loan offers and evaluating the complete cost structure can help you select a loan that suits both your financial needs and budget.

Conclusion

Processing fees are an essential component of personal loans and are charged for evaluating and approving loan applications. In addition to processing fees, borrowers should be aware of foreclosure charges, late payment penalties, EMI bounce fees, and applicable taxes. Before applying for a personal loan, take the time to understand all charges, compare lenders, and review the terms carefully. A clear understanding of these costs can help you manage your finances effectively and choose the most suitable loan option.